Written by: Simon Figures, SC Ventures San Francisco

In Brief

- The metaverse is best described as a future version of the Internet where people interact socially and professionally in persistent, shared, and immersive virtual worlds.

- Numerous analysts are predicting a multi-trillion-dollar opportunity with far reaching implications for a broad range of industry segments.

- Blockchains form the backbone of the metaverse and may enable digital assets – often Non-Fungible Tokens (NFTs) – to be used across different virtual worlds.

In Numbers

Introduction

“The next generation of consumer companies will have business models that resemble Fortnite more than they resemble Facebook.”

Rex Woodbury, Index Ventures (07/20)

As a greater share of our lives are spent connected to others through technology it is increasingly difficult to make a meaningful distinction between our ‘real life’ and our ‘digital life’. 76% of consumers already report that their daily lives and activities depend on technology and a recent McKinsey study estimated that Covid had accelerated by as much as 7 years the development of digital products and services across work, education, commerce and social interaction.

Key elements of this digital wave are rapidly converging, and the contours of a unified, immersive digital future are starting to emerge. The concept of the “Metaverse”, a digital realm that enables people to interact and work in virtual spaces, is not new but has recently seen a surge of attention from consumers, corporates, and investors. In a message to its clients in January 2022, Goldman Sachs predicted the Metaverse would represent an $8 trillion opportunity[1] while a month later, JP Morgan estimated the opportunity as $1 trillion in annual revenues, with virtual worlds “infiltrating every sector in some way in the coming years.”

Adding credence to these predictions have been the flurry of strategic moves by large tech companies; Facebook’s groupwide rebranding to “Meta”, Microsoft’s $75 billion acquisition of videogaming company Activision Blizzard and increasing evidence of an Apple AR/VR headset to name just a few. Altogether, multiple market signals point to a paradigm shift towards a more connected, immersive digital future.

In this report, we attempt to demystify competing visions of the metaverse, identify the potential impact on existing business models, and highlight strategic opportunities for Standard Chartered and as well as for our clients.

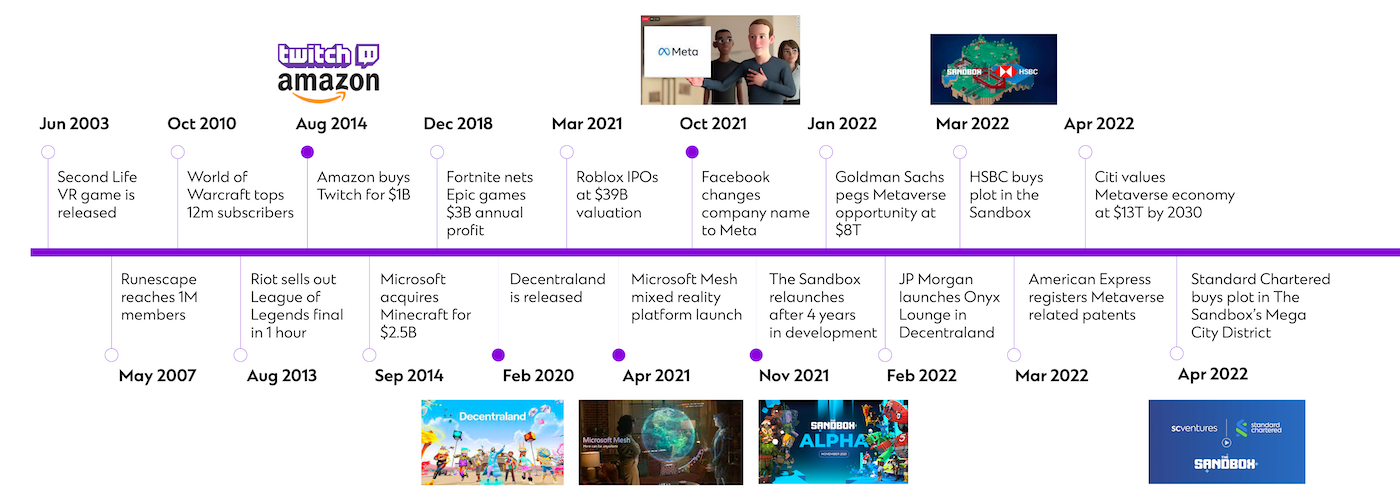

Brief History & Evolution of the Metaverse

What is the Metaverse?

“Just as it was hard to envision in 1982 what the Internet of 2020 would be…we don’t really know yet how to describe the Metaverse.”

Matthew Ball, US Entrepreneur, and Investor

“I see the Metaverse as the gradual convergence of the digital world with the physical world. A world where we no longer notice a distinction between our digital avatars and our physical selves. This is the next iteration of the internet. And as dystopian it may sound, this is the next iteration of life.”

Ryan Gill Cofounder & CEO of Crucible

Innovation does not travel in straight lines and a common understanding of the terms used to describe a new category often lags what can be seen ‘in the wild’. This applies to language used to describe the Metaverse today and is driven in part by different companies using the same terms to stake a claim to their vision of the future.

While we can start to describe the metaverse in terms of things which are becoming more commonplace, for example virtual reality headsets, the graphic below lays out a broader set of attributes which commentators predict are required for a fully realized metaverse.

Figure 1. Key Characteristics of the Metaverse

While almost all visions of the metaverse assume some kind of immersive audio-visual experience, many of the other attributes highlighted above are at a very early stage or yet to be realized.

What are the competing visions of the metaverse?

One of the biggest questions is whether the metaverse will be “centralized” – powered by private platforms such as Facebook or Epic Games (the creators of the popular game Fortnite) or “Decentralized” – built and owned by public users on open protocols such as Decentraland or The Sandbox.

In a centralized metaverse, a single entity would govern the experience, define who has access and likely capture most of the value generated on a specific metaverse platform. This of course leaves open the possibility of there being multiple different competing metaverses.

In a decentralized metaverse, the platform is built on open-source software and governed by community members (users), who have the freedom to design the platform collaboratively and make decisions about the future direction it might take.

Community governance may seem fanciful but Decentralized Autonomous Organizations, known as DAOs, do exist at scale – most notably within Decentralized Finance (DeFi) – lending some credibility to this notion.

As corporate and consumer activity grows, the ranking of centralized vs. decentralized metaverse visions will likely change, although, it is too early to tell whether the trend towards decentralization, which ultimately fueled the growth of Web 1.0 after a centralized first inning, will prevail.

How close are we to a paradigm shift?

What needs to be true?

Many believe it will take years for the enabling technologies and conditions to develop for widespread adoption of a fully realized metaverse. Whether it takes three years or ten, however, sufficient momentum is building for many corporate strategy teams to be investigating what the impact might be.

There will be no clean ‘Before Metaverse’ and ‘After Metaverse’, instead, it will emerge over time as different products, services, and capabilities evolve. This journey is unlikely to be linear, with the last 12 months representing a notable period of rapid acceleration.

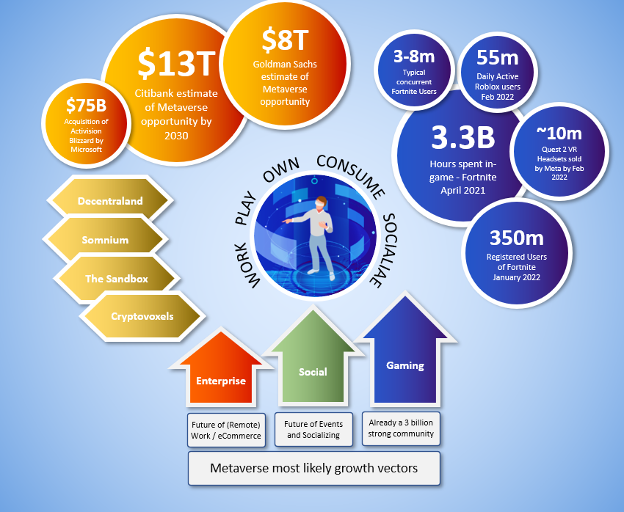

What are the likely growth vectors?

There are competing views on how the metaverse will most likely grow; Gaming, Enterprise adoption and Social networks are generally considered to be the most likely vectors.

Gaming platforms such as Fortnite and Roblox are starting from a position of significant strength. Immersive games and their corresponding ecosystems (such as World of Warcraft, Call of Duty, and Diablo) are massive franchises that have fully established virtual worlds and communities.

To give a sense of scale, Fortnite is currently home to over 350 million registered users and frequently hosts 8 million concurrently; Roblox, another popular gaming platform which went public in 2021 reported over 55 million daily active users on its platform in February 2022.

The respective communities of Fortnite and Roblox can interact on their individual platforms, but they have limited ability to control, own or share in the revenue from the digital worlds they inhabit and are effectively separate technological silos.

On the enterprise software front, Microsoft aims to lead what it calls “the enterprise metaverse” through initiatives such as Microsoft Mesh[2]. CEO Satya Nadella is likely to use Microsoft’s $75 billion acquisition of Activision Blizzard to lead in the content, talent, and community war. In a Microsoft-powered metaverse secular shifts around remote work and the evolution of immersive collaboration tools e.g., Microsoft Teams are front and centre.

Lastly, Meta (formerly Facebook’s) vision of “helping to bring the metaverse to life” appears to be gaining traction. Facebook, as the pre-eminent global social network, is obviously well-positioned particularly given their ownership of the VR hardware company Oculus. The Oculus Quest 2 headset costs around $300 and is estimated to have sold 10 million units in the last 12 months – notably outselling Microsoft’s Xbox gaming console. On the social networking giant’s shift towards a new metaverse-focused vision, CEO Mark Zuckerberg shared the following sentiment: “We believe the metaverse will be the successor to the mobile internet…We’ll be able to feel present – like we’re right there with people no matter how far apart we actually are.”

With continued innovation in metaverse-related hardware by multiple different companies, we will likely see new devices that accelerate user adoption. Rumors of an Apple VR headset have circulated within the tech community for several years. The device may be as light as an iPhone (about 150 grams) which, if true, will be less than a third of the Quest 2 and other competing brands and will expand the number of viable use cases.

How might consumer behavior shift in a metaverse-enabled world?

According to consumer investor Rex Woodbury of Index Ventures, “the next generation of consumer companies will have business models that resemble Fortnite more than they resemble Facebook” and there is growing evidence that consumers are positive about a move from digital experiences to immersive experiences with the tendency increasing after their first immersive experience.

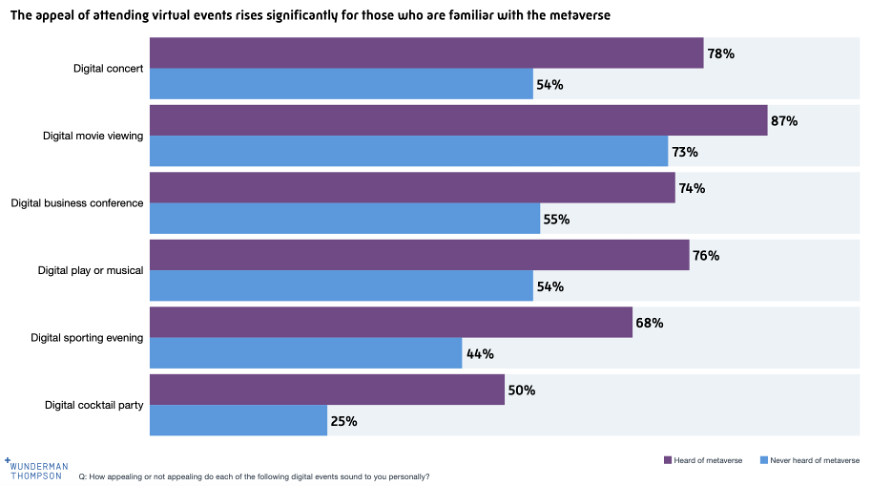

For example, in a recent survey gauging the appeal of virtual events, respondents familiar with the metaverse were significantly more likely to favour virtual events compared with those who were unfamiliar with the concept.

Figure 2. Shifting consumer attitudes towards future digital experiences in the metaverse (Wunderman Thompson)

In one example, popular videogaming platform Fortnite demonstrated massive success in hosting virtual concerts. In December 2019, 3 million people watched a Star Wars event hosted by JJ Abrams and in April 2020 28 million people “attended” a concert by musician Travis Scott. In these events, players have the option to engage with the platform as their favorite characters. Woodbury notes that corporates have been eager to offer free virtual assets in exchange for brand affinity; For example, Disney partnered with Fortnite to introduce Marvel “skins” and the US National Football League (NFL) provided . Both virtual assets were offered for free. Corporations and celebrities are also continuing to explore in-game presences as promotional tools, akin to appearances or performances on traditional talk shows.

The metaverse is a powerful tool for corporates to connect with users as these experiences offer something more than the passive consumption of media we are accustomed to today. According to Alexander Fernandez, CEO and co-founder of Streamline Media Group, “[immersive experiences] take you to another world, bring a sense of wonder and require a suspension of disbelief. It’s psychologically more engaging.” Additionally, the immersive experience removes the distractions of the physical world and enables users to be transported to settings where they can be “fully engaged.”

Digital Goods

Consumers are shifting to view digital goods as comparable to physical goods and prefer digital, immersive shopping experiences

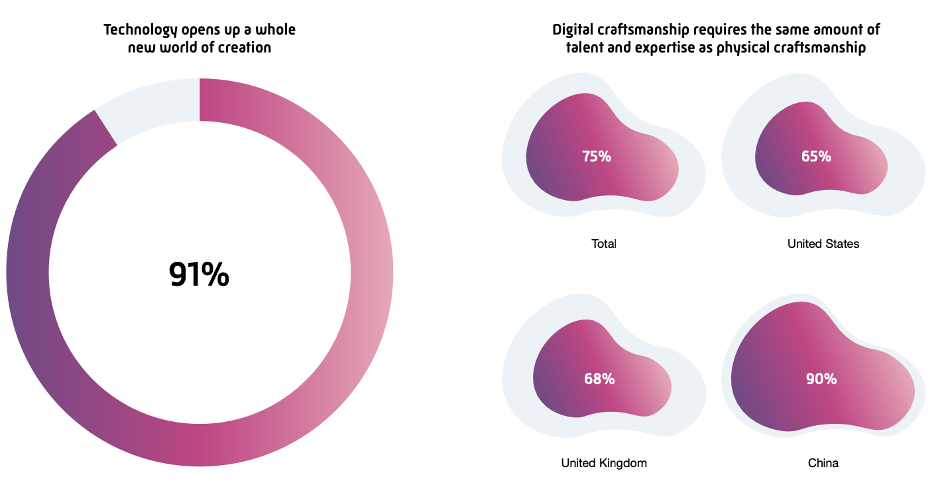

According to a survey by Wunderman Thompson Intelligence, 75% of respondents believe that digital craftsmanship requires the same expertise as physical craftsmanship. This belief is shared by respondents across multiple geographies with China scoring the highest.

Figure 3. Shifting consumer attitudes towards digital craftsmanship (Wunderman Thompson)

Figure 3. Shifting consumer attitudes towards digital craftsmanship (Wunderman Thompson)

This attitude is even more evident amongst younger cohorts who display preferences for digital shopping over in-store experiences. Neha Singh, CEO of Obsess (a virtual store platform that assists brands like Ralph Lauren and Tommy Hilfiger to create virtual shopping destinations) states that “data indicates that the majority of younger consumers want to be able to shop their favorite brands anywhere they go online, including on metaverse platforms…These shoppers have grown up with online videogames, esports and social media and many of them see the emerging metaverse as a modern-day mall—a connected virtual world where they can hang out, shop and socialize. For retail brands, these survey findings highlight the importance of creating sound metaverse commerce strategies today that will resonate with consumers over the coming years.”

Consumers seem to be responding positively to immersive, social commerce models. These models, such as China’s Pinduoduo, enable new ways for consumers to shop with their friends and provide immersive, gamified experiences. In a recent example, the department store wing of South Korea’s retail giant Lotte Group announced a partnership with software developer Vaiv to create a metaverse version of their store.

Many also believe there is massive potential for immersive shopping experiences in travel and hospitality. Virtual reality tools will enable consumers to feel and experience prospective destinations. For example advertising agency Whitespace’s award-winning AR portal for VisitScotland enabled potential tourists to experience the country using virtual reality.

What “Real World” examples of adoption are there?

Marketing and Brand building

In addition to the recent headlines from Meta and Microsoft we are also seeing examples of companies incorporating the metaverse in numerous subtle, yet strategic ways.

New Business Lines: In December 2021, sportswear brand Nike announced its acquisition of RTFKT (pronounced ‘artefact’), a digital design studio producing trainers and other collectibles that can be worn across different online environments. In this way, Nike intends to diversify its products into the metaverse, potentially ramping up its own production of virtual wearables.

Enhancing Corporate-Consumer Relations: As metaverse expert Cathy Hackl notes: “brands will need to continue adapting to relationship styles of play and interactions. Customers won’t just be able to talk to brands as they do today on social media, they’ll be able to interact with them in 3D form.” For example, in August 2021, French fashion house Louis Vuitton (LV) celebrated its founder’s 200th birth anniversary by a mobile game called LOUIS THE GAME. The brand created its own story and world to explore, mimicking a role-playing game (RPG). Furthermore, in January 2022, Ralph Lauren CEO Patrice Louvet stated that the company’s participation in the virtual world helps it connect with younger shoppers, and it subsequently participated in metaverse platform Zepeto and Roblox, where shoppers can dress their avatars in Ralph Lauren apparel.

Community Building: In September 2021, Vans partnered with Roblox to launch “Vans World”, a persistent 3D skate park that allows users to compete, connect with others, design virtual skateboards and Vans shoes. The virtual skate park has attracted over 50 million visitors and has allowed Vans to generate an additional source of revenue through the sale of virtual items.

Experiences: As mentioned above, through the corporate partnerships developed with Fortnite and musical artists, multi-million-dollar opportunities exist for corporates to connect with consumers through virtual events and experiences. Corporates are now exploring how different types of social gatherings, immersive education, travel, and other untapped experiences can complement existing business activities.

Brand Protection and Digital Asset Ownership: Another indicator of companies embracing the metaverse is seen by the increased number of trademark registrations being filed with the US Patents and Trademarks Office, and their foreign equivalents. These applications seek to extend trademark protection over use of the applicant’s brand in the virtual world and in the virtual goods and services that they intend to offer in the Metaverse. The applicants span a wide number of industries and examples of companies who have registered, or are seeking to register, their trademarks, include Nike, Ralph Lauren, Walmart and McDonalds. There is also heightened awareness in relation to other intellectual property considerations relating to the creation, sale and use of digital assets. These include the need to watch out for licensing arrangements and ownership rights over the digital assets, particularly where the digital asset is created as part of a collaboration or where it may be commercialized or exploited. While enforceability of rights over digital assets still remain uncertain, there are an increasing number of cases being brought involving unauthorised use of a brand’s trademarks (such as in the recent lawsuit filed by Hermes against Mason Rothschild involving Hermes’ popular “Birkin” bag). These are currently being disputed with significant interest in what their outcomes are going to be.

Digital space: metaverse real estate

“Virtual worlds have been destigmatized as a result of COVID in a truly unique way. COVID has legitimized time in virtual worlds in a way that almost no other event could have.”

Matthew Ball, Metaverse VC & Essayist

There has been accelerated interest in the concept of digital real estate in recent years. Imagine a digital twin of the physical world, in which you can explore, engage, and interact with others using augmented & virtual reality devices.

While still in the earliest stages, investment into the metaverse real estate market has drawn the fascination of the public as early investors commit significant amounts of money to digital land. In 2021, CNBC reported $500 million was invested into metaverse real estate, an amount projected to double this year.

Most of this activity is concentrated into the “Big Four” platforms: Decentraland, Sandbox, Cryptovoxels and Somnium. These platforms have dominated the market, and together represent a total of 268,645 virtual land parcels, all of varying sizes.

| Platform | Founded | Developer(s) | Users | Virtual Land Parcels | Coin |

| Decentraland | 2015 (launched 2020) | The Decentraland Foundation | 8.5 million (Dec 2021) | Fixed at 90,601 | MANA |

| The Sandbox | 2011 (re-launched in 2021) | Animoca Brands (Hong Kong) | 2 million (March 2022) | Fixed at 166,464 | SAND |

| Cryptovoxels | 2018 | Nolan Consulting (New Zealand) | ~9,000 (Sept 2021) | Unlimited (7,351 as of Feb 2022) | ETH |

| Somnium | 2017 (launched 2018) | Artur Sychov (Czech Republic) | ~4,600 (March 2022) | Fixed at 5,025 | CUBE |

Figure 4. Comparing the four most popular virtual land platforms today

Decentraland, an open-source 3D virtual world platform founded in 2015, allows users to place 3D models in a digital space using a simple drag and drop builder tool. Professionals can generate interactive content and code advanced applications, games, and animations. With a fixed 90,600 parcels on the platform, users can invest in parcels that are expected to appreciate over time. In December 2021, Tokens.com spent a record-breaking $2.4 million for 116 parcels in Decentraland’s fashion district, where the company plans to host fashion events and retail shops. Decentraland is one of the oldest Metaverse platforms and has collaborated with Samsung and the Australian Open (AO) in the past.

Similarly, The Sandbox, a leading decentralized gaming virtual world, has gained much recent attention. In January 2022, the company announced it was working with multiple partners in the entertainment, finance, gaming, real estate, and Hong Kong film industry to create a virtual Mega City, which will be “will be a cultural hub based on or inspired by multiple Hong Kong talents”; Standard Chartered itself announced a partnership with the Sandbox and the purchase of land in Mega City in April 2022[3].

Remote work and the evolution of the office

The current virtual office environment has been the most popular office for many in recent years. As the global pandemic accelerated the development of fully remote or hybrid work settings, employers and employees have had ample amounts of time to rethink the nature and importance of the physical office. As workers look to more immersive work environments in the future, AR/VR solutions such as Spatial are paving the way to a true metaverse workforce.

As Ben Thompson writes, the metaverse can play a key role in enabling the Future of Work: “Think again over the last couple of years: most of those people working from home were hunched over a laptop screen; ideally one was able to connect an external monitor, but even that is relatively limited in size and resolution. A future VR headset, though, could contain as many monitors as you could possibly want — or your entire field of view could be one massive monitor. Moreover, the fact that a headset shifts your senses out of your physical environment is actually an advantage if said physical environment has nothing to do with your work.”

Potential Impact

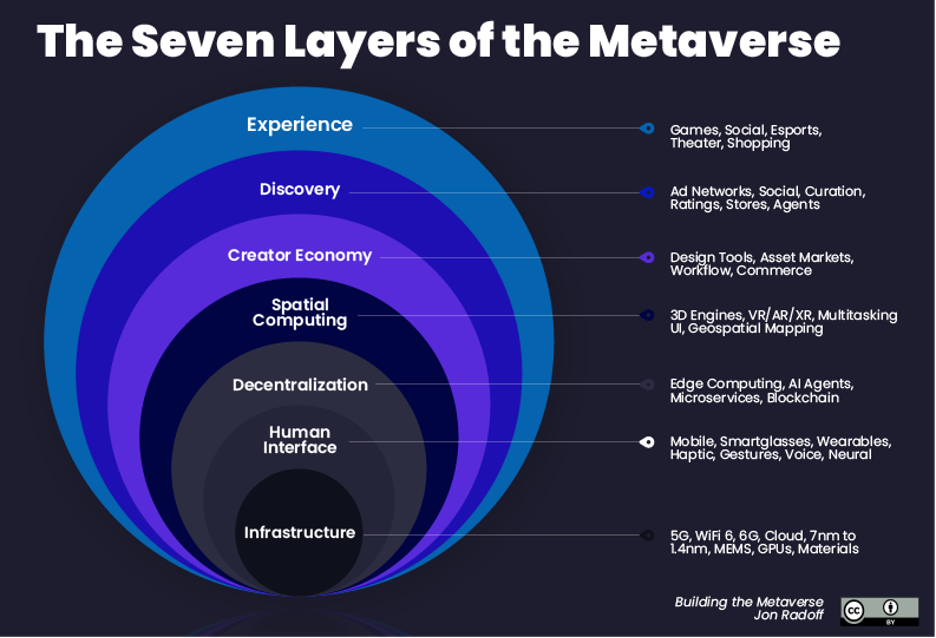

Figure 5. The Seven Layers of the Metaverse (Jon Radoff)

Figure 5. The Seven Layers of the Metaverse (Jon Radoff)

Jon Radoff, CEO of gaming startup Beamable provides a helpful framework that breaks down the metaverse down into 7 different layers in which we are seeing companies operate:

- Experience: This is the most obvious layer to consumers – users interact in digitally driven environments through content such as games, shopping, NFTs, e-sports and events.

- Discovery: This refers to the push and pull process of introducing new experiences to users. Generally, discovery can be classified as either inbound (app stores, search engines for reviews and ratings) or outbound (notifications and display advertising).

- Creator economy: The creator economy layer refers to the design tools, marketplaces, and workflow platforms used by creators to build and release metaverse worlds, experiences and assets.

- Spatial computing: Technologies such as AR, VR, extended reality (XR) and space mapping fall under this layer – which is central to blending the physical and virtual.

- Decentralisation: This covers both the hardware decentralization – required for high resolution experiences – and decentralization of ownership via blockchains.

- Human interface: The technology allowing our physical body to interact with the digital world.

- Infrastructure: The underlying technology, storage, compute and distribution that powers the metaverse.

Financial Service Impact

In the financial services industry there are an increasing number of ways in which the metaverse may impact existing business models and spur new ones.

Investment Products: As digital assets become central to metaverse presence and activity, asset managers are increasingly interested in enabling their customers to invest in this new category. Enabling technology such as MetaMask Institutional is making it easier for corporates, family offices, and financial institutions to integrate with the asset rails used within these worlds thereby driving access and growth. Standard Chartered’s Zodia, one of the first institutional-grade custody solutions for crypto currencies is already exploring how to support a broader range of digital assets. Additionally, metaverse ETFs (such as the Roundhill Ball Metaverse ETF) and the concept of metaverse real estate mortgages have made headlines.

Client Experience: The immersive nature of metaverse technologies allow financial firms to connect with clients in new ways. For example, South Korean KB Kookmin Bank launched, KB Financial Town, a virtual version of a traditional bank branch. Furthermore, results from a 2020 study conducted by University College Dublin testing the effectiveness of VR uses on communication in financial services (as opposed to video conferences) pointed to improved feelings of presence and closeness by the participants.

Metaverse Finance (“MetaFi”): Today’s nascent digital creator economy, which includes publishing, gaming (skin creation), digital art, streaming, music and more, is home to over 50 million content creators. These artists create digital goods and are often paid in digital tokens which are exchanged within an emerging digital asset economy. We have seen early examples of these markets through the growth of NFTs (Non Fungible Tokens) representing land and assets as well as “in game currencies” such as Robux. This new economy heralds new kinds of financial services described as “MetaFi” and is a natural place for existing financial services companies to explore.

Strategic Opportunities

“When I think about the bank of the future, I often think about my sons and how they play Fortnite with their friends.”

– Derek White, BBVA’s Global Head of Client Solutions (April 2020)

In addition to activities by banks such as Goldman Sachs and Morgan Stanley, many other financial firms have signaled their interest in the metaverse.

In February 2022, JP Morgan announced its “Onyx Lounge” in Decentraland, and released a paper explaining the metaverse opportunities they are exploring.

Banco Santander and BBVA indirectly made their debut in the Decentraland metaverse in February 2022 as joint shareholders in the developer Metrovacesa. Metrovacesa and Datacasas Proptech, a Spanish startup specializing in the online sale of properties, plans to market digital real estate in the metaverse.

In November 2021, HSBC joined a $200M funding round for ConsenSys, a blockchain software engineering firm, that notably owns MetaMask Institutional, a solution which will allow corporates to integrate with digital assets more easily.

SCB (Siam Commercial Bank) through their innovation arm SCB10X opened the doors to their Sandbox property in March 2022 at the same time as announcing a $600m digital asset fund and metaverse creation studio.

Lastly, in January 2022, DBS held its H1 2022 Market Outlook entitled “Into the Metaverse”, where the firm explored top emerging investment trends. CIO of Consumer Banking & Wealth Management Hou Wey Fook examined the questions of whether the digital economy will be potentially larger than the physical one.

Conclusion

With any paradigm shift, it can be difficult to separate valid signal from speculative noise. Over the past two years we argue, the metaverse signal to noise ratio has improved with concrete investments, software maturity, hardware improvements and consumer awareness all increasing. Consequently, many corporates are now trying to work out “how” the metaverse will impact their business, not ‘If”.

Changing consumer behavior complemented by rapidly developing technology are strongly signaling that our future social and professional lives including how we earn, spend, and invest our money will become increasingly immersed in virtual worlds.

It was not so long ago that consumers were baffled by the investment in .com addresses in the same way many are today with purchases of digital land. With only a relatively short 40-year history, the internet looks set to evolve again in ways that will radically change how we live and work.

[1] These figures represent the midpoint of Analyst estimates of the rapidly growing digital economy as a proxy for the metaverse.

[2] Microsoft Mesh https://www.microsoft.com/en-us/mesh

[3] https://scventures.io/standard-chartered-partners-with-the-sandbox-to-create-metaverse-experience/

Appendix

Disclaimer

This document is prepared and issued by SC Ventures, a division of Standard Chartered Bank (“SC”) that invests in disruptive technology and explores alternative business models for SC. SC (incorporated with limited liability in England by Royal Charter) is authorised by the Prudential Regulation Authority (“PRA”) and regulated by the PRA and the Financial Conduct Authority.

It is provided for information purposes only. It is not intended, and should not be relied upon, as advice on the regulatory, accounting or other treatment of any topics presented herein. It is not intended to offer recommendations or advice (including but not limited to any recommendations or advice in relation to investing in or purchasing digital assets) nor to sell any product or provide any service. SC does not provide accounting or regulatory advice and recommends that you seek advice from your own lawyers, accountants, auditors and/or other professional advisers (“Advisors”).

While reasonable care has been taken in preparing this document, SC, its affiliates and its and its affiliates’ directors, officers or employees (the “SC Group”) does not accept any responsibility or liability of any kind with respect to the accuracy or completeness of the information contained in this document or for errors of fact or for any opinion expressed herein. Accounting laws, rules, regulations, standards and other guidelines may differ in different countries and/or may change at any time without notice. The SC Group is under no obligation to update the document or to inform you or anyone else about any change (whether or not known or apparent to the SCB Group) to the information in the document.

This document is provided to assist interested parties in making a preliminary analysis of the topics presented herein and does not purport to be all-inclusive or to contain all of the information that you may require to make a full analysis of the topics. It is for information and discussion purposes only and does not constitute either an offer to sell or the solicitation of an offer to buy any digital asset, security or any financial instrument or enter into any transaction or recommendation to acquire or dispose of any investment.

Information (including summaries of regulations) appearing herein has been obtained from various public sources believed to be reliable. We do not represent or warrant that this information is accurate or complete. Accordingly, it should not be relied upon as such. The information contained herein does not purport to identify or suggest all the risks (direct or indirect) that may be associated with conducting business. SC may not have the necessary licenses to provide services or offer products in all countries or such provision of services or offering of products may be subject to the regulatory requirements of each jurisdiction and you should check with your Advisors before proceeding. You are expected to exercise your own independent judgment (with the advice of your Advisors) with respect to the risks and consequences of any matter contained herein. We expressly disclaim any liability and responsibility for any losses arising from any uses to which this document is put and for any errors or omissions in this document.

© Copyright 2022 Standard Chartered Bank. All rights reserved. All copyrights subsisting and arising out of these materials belong to Standard Chartered Bank and may not be reproduced, distributed, amended, modified, adapted, transmitted in any form, or translated in any way without the prior written consent of Standard Chartered Bank.